For many non-US founders, forming a US startup is the same as it is for US founders: incorporate a Delaware corporation, issue founder stock, file an 83(b) election, get an EIN, open a bank account. Plenty of founders living outside the US can follow that exact path with no trouble.

But for others, it isn't that simple. Depending on where a founder lives, tax regulations, immigration law, and currency controls can make the standard approach unworkable. Until now, founders in this position have been doing one of two things: working with an attorney or using an online legal service marketed toward non-US founders.

Working with an attorney who has the right country-specific experience is an excellent approach. Two things have made it hard, though. First, very few attorneys specialize in any one country's cross-border formation, so finding the right one is difficult. Second, the rare attorney who does this work has had no easy way to streamline it, which has kept the process manual and time-consuming.

The other approach has been to use an online legal service marketed toward non-US founders. The problem is the paperwork they produce for non-US founders is the same as what they produce for US founders.

Our Solution

We've been bothered by this status quo for years and are pleased to introduce our solution: the ability for country-specific experts to build custom online legal services for specific situations, using Clerky products as modular building blocks. It's finally possible to combine country-specific expertise with the speed and accessibility of an online legal service.

These services can include the same products US startups use by default on Clerky. They can also choose from a selection of products designed for less common scenarios, previously available only to law firms.

This new approach also benefits from the unique infrastructure we have for non-US founders. As an example, these custom online legal services can integrate our Managed 83(b) Election add-on. This is the only way non-US founders can obtain USPS-postmarked certified mail receipts for 83(b) elections through an online legal service.

Inkle Incorporate

Inkle is the first to build on this new approach with their launch of Inkle Incorporate, an online legal service for US-India cross-border startups.

Because of tax regulations, immigration law, and currency controls in India, founders of these startups can't safely form a US entity the same way US founders would. So Inkle worked closely with legal and tax specialists in both the US and India to build a custom online legal service for exactly this situation, using Clerky products for the US paperwork.

Inkle is a natural fit for this. It's a tax and accounting platform used by many of the fastest-growing US-India cross-border startups, including half of all YC companies in India. Most Indian companies in YC's S26 batch have already used Inkle Incorporate to form their startups, with more on the way.

We're excited to see where Inkle Incorporate goes from here. If you're an expert interested in building something similar for founders in another country, we'd like to hear from you. Or if you're a startup founder in India and want to form a US entity, check out Inkle Incorporate.

We're excited to share that Lowenstein Sandler has launched a tailored startup formation experience for their clients, built on Clerky. Lowenstein is a national law firm with one of the top 10 most active startup practices in the US. Founders working with Lowenstein can now form their startup online through a co-branded workspace with a curated mix of standard Clerky products and custom Lowenstein products.

Now, when founders work with Lowenstein to form a new startup, their attorney can invite them to a Lowenstein workspace on Clerky. There, they'll get the same underlying software all Clerky startups get, co-branded with Lowenstein's logo and subdomain. Founders can then incorporate, set up their board, appoint officers, issue shares to founders, enter into confidentiality and intellectual property agreements, and adopt a stock plan.

Throughout the experience, Lowenstein attorneys will be available to clients, leveraging Clerky's built-in collaboration features. They can review paperwork, flag issues, and answer questions on the platform, providing clients with legal advice coupled with our software. After completing formation paperwork, Lowenstein clients will also have access to banking integrations and valuable perks for Clerky startups.

We pride ourselves on responsibly leading innovation for startup legal paperwork and are proud to be now helping innovative law firms like Lowenstein lead the way for their clients. Startups and their attorneys are increasingly working together to get legal paperwork done more efficiently, and this is an exciting leap forward in that journey.

Here's what's new:

You can now open a Ramp account and get a cash bonus

Ramp has joined our ecosystem of banking platforms. You can now start an application through Clerky in just one click and get up to $1,750 in bonuses: $1,000 after a $25k Ramp Treasury deposit, plus $750 after your first $1k balance payment (both within 90 days).

IRS EIN processing time tracker for non-US founders

Non-US founders and others applying for an EIN by fax can now check live IRS processing times on Clerky. Our auto-updating status page shows projections based on the applications we process in-house, providing you the most accurate estimate available.

New and updated perks

- Google Workspace — 20% off for the first 6 months

- Inkle — Updated: 25% off bookkeeping for 6 months, plus free FBAR, Form 7004, and Form 1099 filings when you subscribe to Inkle Tax Standard and use Inkle to file Form 1120

- Xero — 6 months free

You can view these perks by going to Perks for your team.

You can now start a Ramp application in one click, right through Clerky. Ramp will even pre-fill the form with information from your legal paperwork to save you time. And once your account is open, we'll store your wire instructions so they're ready to go when you raise your seed round.

To celebrate, Ramp is offering Clerky startups up to $2,000 in cash bonuses. You can earn $1,500 when you deposit $250k or more in Ramp Treasury and spend $10k on your Ramp card within 90 days (or just deposit $750k or more in Ramp Treasury). You can then get another $500 after your first $1k balance payment.

Here's what startups can get with Ramp:

- No personal guarantee — Ramp underwrites based on your startup's financials, not your personal credit

- 2% APY on a fully liquid FDIC-insured account with Ramp Treasury

- Deep integrations with QuickBooks, NetSuite, Xero, and Sage Intacct

You can start your application today by going to Banking for your team and selecting Ramp.

Here's what's new:

New and updated perks

- Asana — Updated! This perk is now so good they won't let us say more here, but you can find all the details on Clerky.

- Common Paper — New! 50% off first 3 months

- Drata — New! 25% off first contract

- Framer — New! Free for 1 year

- Uber for Business — New! Up to 10% off eligible business rides (5 per employee)

New Maintenance product for PBC startups

PBC startups on Clerky can now change their corporate name, number of authorized shares, or par value even before they have directors. This product is available to PBC startups by request as well as to all Attorney accounts. If your startup is a PBC and you'd like to use this, please reach out to our support team.

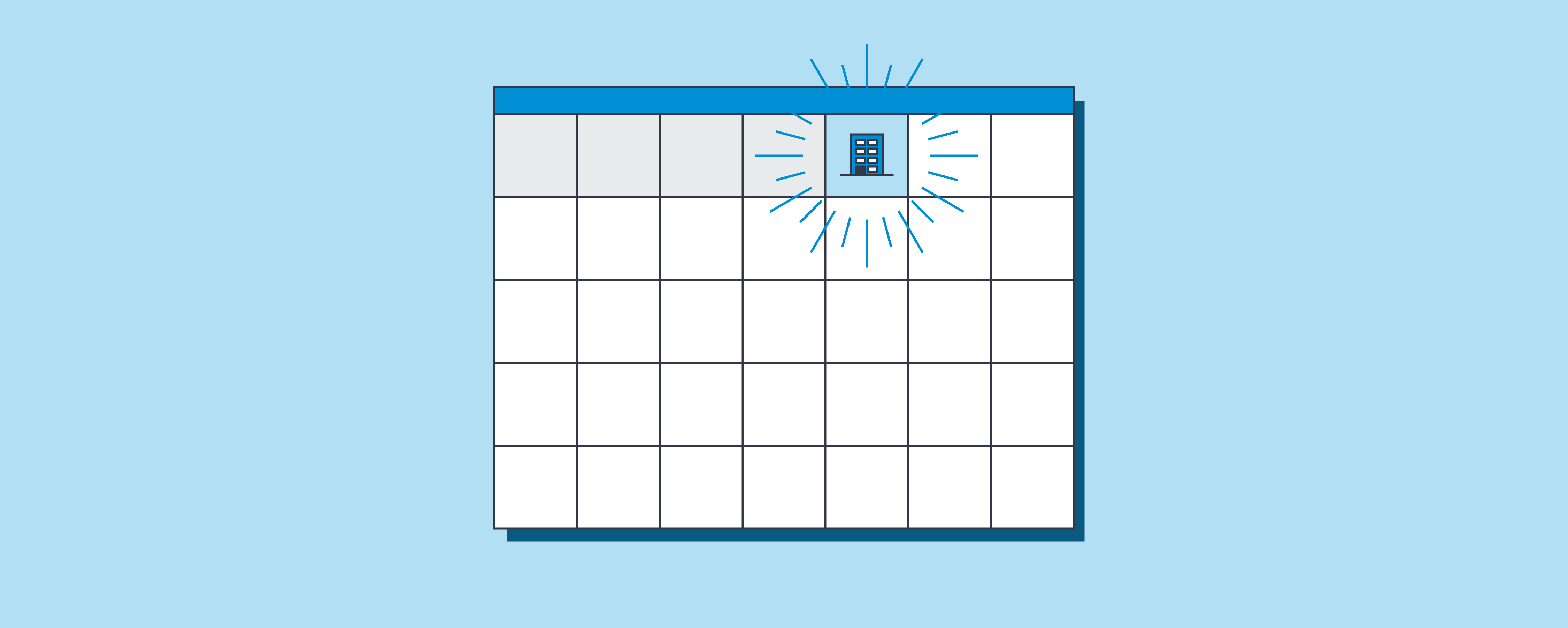

If you're incorporating a new startup soon, you might be able to save around $400 by avoiding the 2025 Delaware franchise tax.

Delaware franchise taxes aren't pro-rated, which means that a Delaware corporation incorporating on December 31, 2025 will have to pay the same franchise tax for 2025 as one that incorporated on January 1, 2025. If you have investors ready to wire funds, this probably isn’t a big deal. But if you're not in a rush, it could be a waste of money.

To avoid this, we can help you take advantage of a little-known nuance of Delaware law that allows you to specify the effective date of an incorporation. If you specify January 1, 2026, your corporation won't exist until then, which means it won't need to pay the 2025 franchise tax. This feature is available to all our customers at no extra charge.

Of course, you won't be able to do other legal paperwork or open bank accounts until the incorporation is effective. So why not just wait until January 1 to submit your incorporation paperwork? Two reasons:

You want to make sure no one else takes your startup's name.

It can feel like a minor miracle to find a name you like that isn't already taken. By filing your incorporation paperwork, you can secure the name you want when the filing is accepted, even if the incorporation won’t be effective until later. You could reserve the name instead, but that adds unnecessary expense and complexity.

You want to hit the ground running in 2026.

Maybe you’ve decided to wait until after the end-of-year holidays to focus on your new startup. Filing your incorporation paperwork before you ring in the new year will save you time in 2026.

In addition, the start of a new year can be busy for the Delaware Division of Corporations, which can lead to delays in processing new incorporations. Filing ahead of time can help you beat the crowds and avoid those delays.

We've made January 1 effective date incorporations available to startup founders for many years, and are excited to bring them back again. From now until the end of the year, you can have your incorporation take effect on January 1, 2026 when you incorporate a new startup on Clerky.

.png)

Of course, if you prefer, you can still choose to have it take effect immediately when the Delaware Division of Corporation files it.

To get started, sign up for Clerky now. Questions? Feel free to reach out!